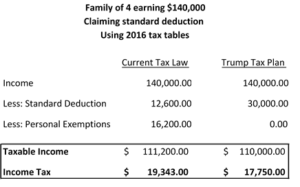

Trump tax – Business

We hope you enjoyed our initial installment last week, where we covered the likely changes associated with the Trump tax plan. Specifically, we covered how the Trump tax plan may impact individuals. In the second part of our examination of the Trump tax plan we reviewed proposed changes in tax policy for business taxes.

Some of the largest cuts in the Trump tax plan are reserved for business taxes.

The top corporate tax rate would fall from 35% to 15%. This lowering of the corporate tax structure would make corporate taxes much more attractive under certain circumstances by reducing the effect of double-taxation of corporate profits. This is especially true when you consider that the current capital gains and dividends rates are much lower than historical rates.

In a major shift of tax policy, the owners of pass-through entities, such as sole proprietorships, DBA’s, partnerships, and S-corporations, could elect to be taxed at a flat rate of 15% on their business income rather than “regular” individual income tax rates. This change could make a big difference. We will use one example. Let’s say you have the option to go to your employer and ask to be treated as a subcontractor going forward. If your normal “highest” tax rate is 33%, if you elected to pay the flat 15% rate, you might be able to save up to 18% in federal taxes by changing the structure of your income. While it is too soon to know if this change will go through, it will be important to keep an eye on this tax change alone!

The Trump tax plan also contains a strategy to decrease the incentive for a US company to “move” its tax residence overseas. Currently a 35% tax rate is applied to companies that wish to repatriate cash held overseas. The Trump tax plan would impose a one-time tax of 10% on the repatriation of cash to the US. This shift in tax policy should increase cash available for reinvestment and dividends in the US.

Businesses engaged in manufacturing could also elect to expense investment in equipment rather than depreciating the cost over time. If this election is made, the business would not be allowed to deduct interest expenses on their business return.

Available documents describing the Trump tax plan also imply many business credits would be repealed. Specifically, the research and development credit would be retained and the credit for employer-provided child and dependent care may be expanded. Other credits may be on the table. But, the language is too vague at this point to help provide further guidance one way or the other.

Thank you for allowing us to nerd out on tax policy. Overall we see some benefits and detractions relating to the proposed changes. So, if you would like more information about how these changes may affect you and your business, feel free to reach out to us by email at [email protected] or 616-822-2981.